Code

D <- read.delim("data/dish.txt") %>%

rename(Year = YEAR)

modDish_ols <- lm(DISH ~ RES, data = D)Here we use time series data (ordered by \(t\)), thus, Equation A.1 will be written with the time indices \(t\) as \[ y_t=\beta_0+\beta_1x_t+\varepsilon_t, \tag{B.1}\] where the regression errors at times \(t\) and \(t-1\) are \[ \begin{split} \varepsilon_t&=y_t-\beta_0-\beta_1x_t,\\ \varepsilon_{t-1}&=y_{t-1}-\beta_0-\beta_1x_{t-1}. \end{split} \tag{B.2}\]

An AR(1) model for the errors will yield \[ \begin{split} y_t-\beta_0-\beta_1x_t & = \rho\varepsilon_{t-1} + w_t, \\ y_t-\beta_0-\beta_1x_t & = \rho(y_{t-1}-\beta_0-\beta_1x_{t-1})+w_t, \end{split} \tag{B.3}\] where \(w_t\) are uncorrelated errors.

Rewrite it as \[ \begin{split} y_t-\rho y_{t-1}&=\beta_0(1-\rho)+\beta_1(x_t-\rho x_{t-1})+w_t,\\ y_t^* &= \beta_0^* + \beta_1 x_t^*+w_t, \end{split} \tag{B.4}\] where \(y_t^* = y_t-\rho y_{t-1}\); \(\beta_0^* = \beta_0(1-\rho)\); \(x_t^* = x_t-\rho x_{t-1}\). Notice the errors \(w_t\) in the final Equation B.4 for the transformed variables \(y_t^*\) and \(x_t^*\) are uncorrelated.

To get from Equation B.1 to Equation B.4, we can use an iterative procedure by Cochrane and Orcutt (1949) as in the example below.

D <- read.delim("data/dish.txt") %>%

rename(Year = YEAR)

modDish_ols <- lm(DISH ~ RES, data = D)#>

#> Call:

#> lm(formula = y.star ~ x.star)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -479.7 -117.8 32.9 120.7 536.1

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 26.76 130.69 0.20 0.84

#> x.star 50.99 7.74 6.59 1e-06 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Residual standard error: 252 on 23 degrees of freedom

#> Multiple R-squared: 0.654, Adjusted R-squared: 0.639

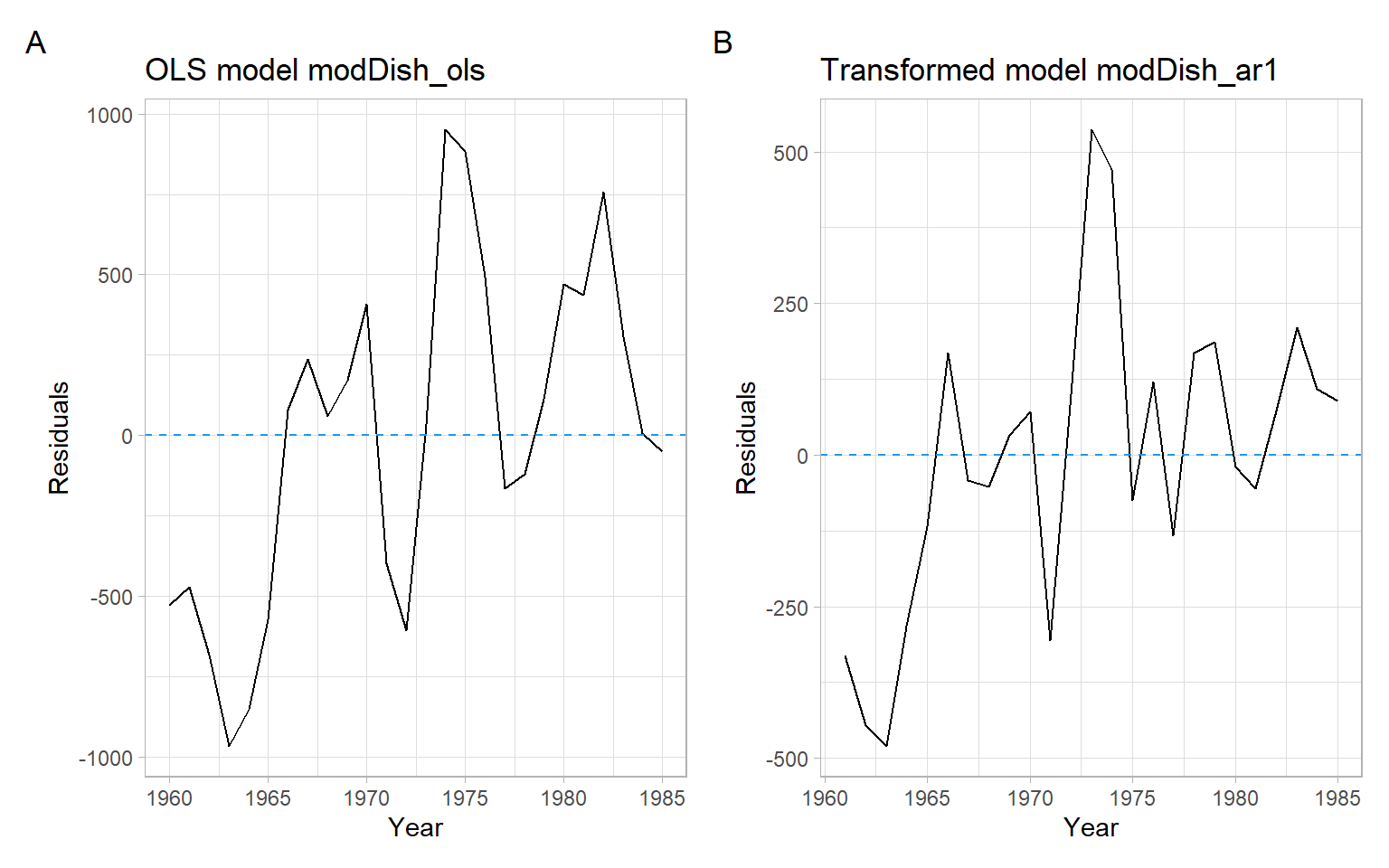

#> F-statistic: 43.4 on 1 and 23 DF, p-value: 1.01e-06p1 <- ggplot(D, aes(x = Year, y = modDish_ols$residuals)) +

geom_line() +

geom_hline(yintercept = 0, lty = 2, col = 4) +

ggtitle("OLS model modDish_ols") +

ylab("Residuals")

p2 <- ggplot(D[-1,], aes(x = Year, y = modDish_ar1$residuals)) +

geom_line() +

geom_hline(yintercept = 0, lty = 2, col = 4) +

ggtitle("Transformed model modDish_ar1") +

ylab("Residuals")

p1 + p2 +

plot_annotation(tag_levels = 'A')

Based on the runs test, there is not enough evidence of autocorrelation in the new residuals:

What we have just applied is the method of generalized least squares (GLS): \[ \hat{\boldsymbol{\beta}} = \left( \boldsymbol{X}^{\top}\boldsymbol{\Sigma}^{-1}\boldsymbol{X}\right)^{-1} \boldsymbol{X}^{\top}\boldsymbol{\Sigma}^{-1}\boldsymbol{Y}, \tag{B.5}\] where \(\boldsymbol{\Sigma}\) is the covariance matrix. The method of weighted least squares (WLS; Appendix A) is just a special case of the GLS. In the WLS approach, all the off-diagonal entries of \(\boldsymbol{\Sigma}\) are 0.

We can use the function nlme::gls() and specify the correlation structure to avoid iterating the steps from the previous example manually:

#> Generalized least squares fit by REML

#> Model: DISH ~ RES

#> Data: D

#> AIC BIC logLik

#> 342 347 -167

#>

#> Correlation Structure: AR(1)

#> Formula: ~Year

#> Parameter estimate(s):

#> Phi

#> 1

#>

#> Coefficients:

#> Value Std.Error t-value p-value

#> (Intercept) -137.5 3714137 0.00 1

#> RES 45.7 6 7.35 0

#>

#> Correlation:

#> (Intr)

#> RES 0

#>

#> Standardized residuals:

#> Min Q1 Med Q3 Max

#> -0.000249 -0.000014 0.000135 0.000232 0.000338

#>

#> Residual standard error: 3714137

#> Degrees of freedom: 26 total; 24 residualIn the function nlme::gls() we can also specify weights to accommodate heteroskedastic errors, but the syntax differs from the weights specification in the function stats::lm() (Appendix A). See ?nlme::varFixed.